Route Mobile Limited (NSE:ROUTE) has announced that it will be increasing its dividend from last year’s comparable payment on the 22nd of February to ₹6.00. Despite this increase, the dividend yield of 0.4% is only a modest boost to shareholder returns.

View our latest analysis for Route Mobile

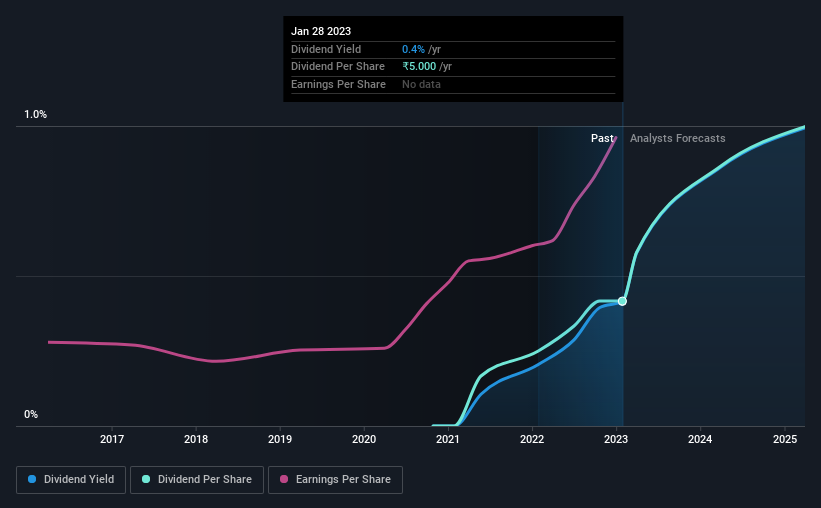

Route Mobile’s Payment Has Solid Earnings Coverage

While yield is important, another factor to consider about a company’s dividend is whether the current payout levels are feasible. However, Route Mobile’s earnings easily cover the dividend. This means that most of what the business earns is being used to help it grow.

Over the next year, EPS is forecast to expand by 64.8%. If the dividend continues along recent trends, we estimate the payout ratio will be 17%, which is in the range that makes us comfortable with the sustainability of the dividend.

Route Mobile Is Still Building Its Track Record

Looking back, the dividend has been stable, but the company hasn’t been paying a dividend for very long so we can’t be confident that the dividend will remain stable through all economic environments. The annual payment during the last 2 years was ₹2.00 in 2021, and the most recent fiscal year payment was ₹5.00. This implies that the company grew its distributions at an annual rate of about 58% over that duration. The dividend has been growing rapidly, however with such a short payment history we can’t know for sure if payment can continue to grow over the long term, so caution may be warranted.

The Dividend Looks Likely To Grow

The company’s investors will be pleased to have been receiving dividend income for some time. It’s encouraging to see that Route Mobile has been growing its earnings per share at 35% a year over the past five years. Earnings have been growing rapidly, and with a low payout ratio we think that the company could turn out to be a great dividend stock.

We Really Like Route Mobile’s Dividend

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Earnings are easily covering distributions, and the company is generating plenty of cash. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Investors generally tend to favor companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analyzing a company. Taking the debate a bit further, we’ve identified 1 warning sign for Route Mobile that investors need to be aware of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we’re helping to make it simple.

Find out whether Route Mobile is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

Do you have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take into account your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.