BanksPhotos/iStock Unreleased via Getty Images

Alpha Pro Tech (NYSE:APT) is a manufacturer of disposable apparel and building insulation materials.

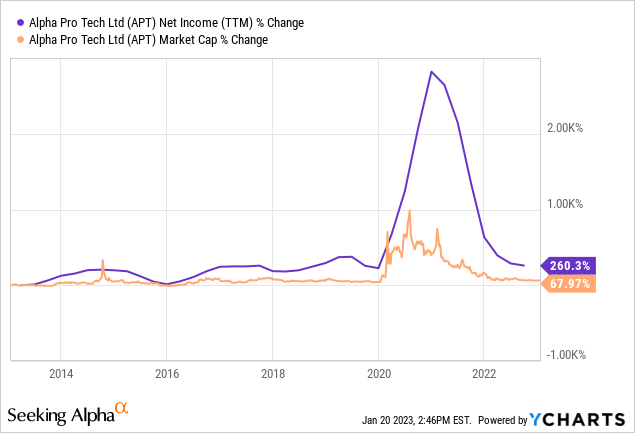

The company saw its profits skyrocket during the pandemic, fueled by the disposable apparel segment. It is now returning to more regular profitability levels. The building materials business is more stable and has been growing consistently. Both businesses are operationally leveraged.

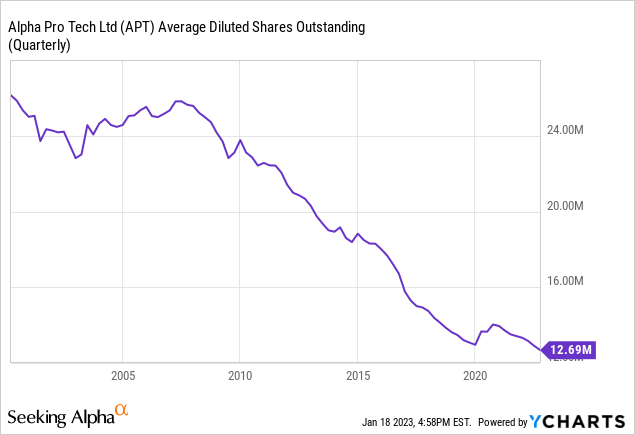

In terms of capital allocation, APT has done aggressive share repurchases, which have halved the outstanding share count in the past 10 years.

Although the company is now trading at a not so high multiple compared to FY22E income, historically it has suffered from big cost lags after an oversupply period like the one the pandemic generated. For this reason, the multiple compared to historical earnings is much higher, and I believe the stock is not a buy.

Note: Unless otherwise stated, all information has been obtained from APT’s filings with the SEC.

Business description

Disposable clothing: This segment manufactures gowns, shoecovers, labcoats, facemasks and faceshields, etc. It manufactures most of its products in the US and a part in India. It is responsible for the company’s tremendous jumps (and then lags) in earnings for the years 2010, 2015 and 2020/21. The segment has averaged a 20% margin before unallocated expenses during normal periods, and has not grown across cycles. This segment had sales of approximately $30 million in 2021, essentially the same level that it generated in 2007, 14 years later.

Building supplies: This segment manufactures and sells insulation materials, particularly housewrap and roof insulation. It manufactures in India for the most part. It has a lower margin, of about 15% before unallocated expenses, but has grown a lot. It had sales of $8 million in 2006, $24 million in 2012, and $37 million in 2021.

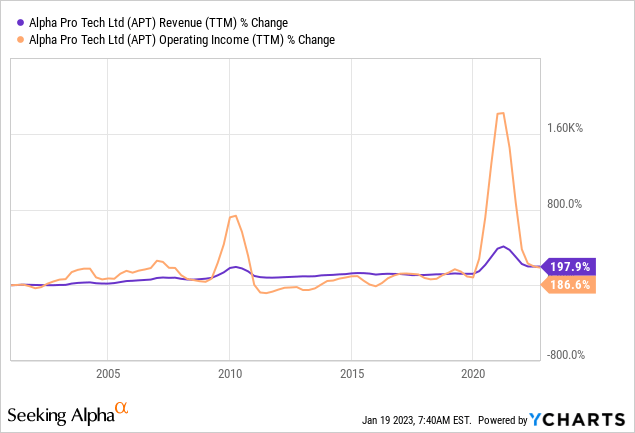

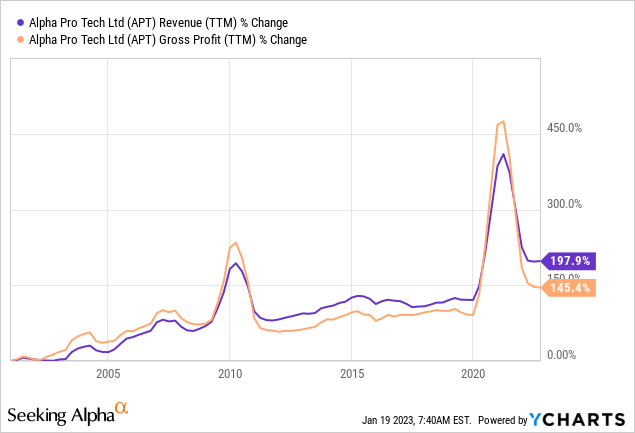

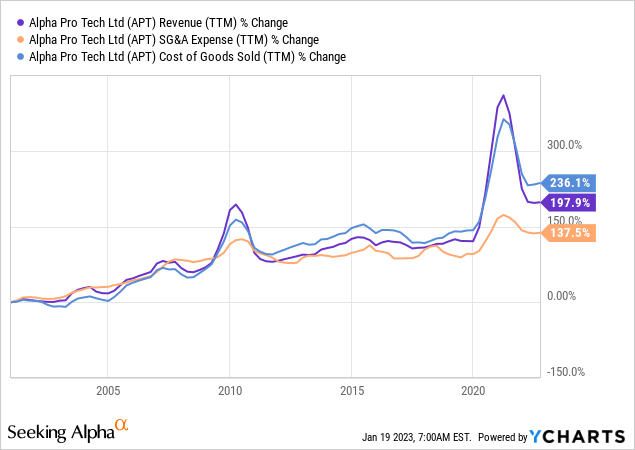

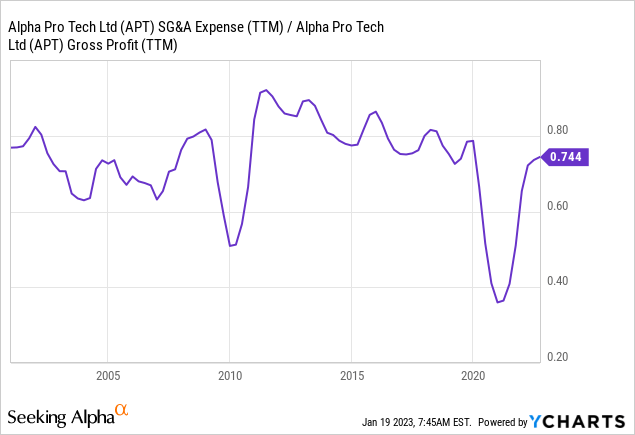

Both businesses have operational leverage: The combined entity shows operational leverage both at the gross (manufacturing) and operating (selling and administrative) level. In the historical record, both businesses suffer from this, although the apparel segment multiplies the phenomenon by its tremendous jumps in revenues during pandemics (2006, 2009, 2020).

Low moat businesses: Despite their high margins before unallocated expenses, and the fact that Building Supplies has grown significantly, none of this business has the characteristics of a defendable business: they produce commodities, that are sold through wholesalers and distributors, purchased by purchase managers at institutions or companies during normal times.

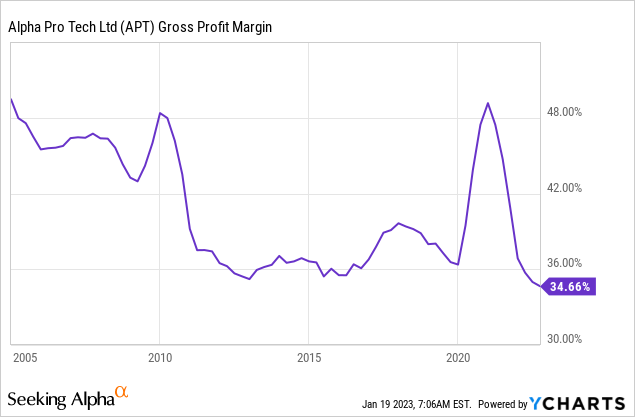

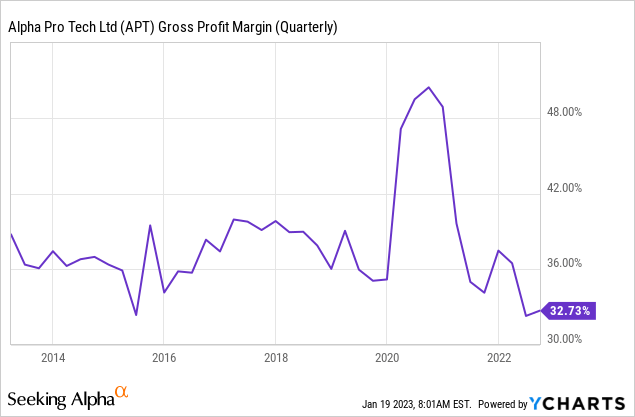

After the oversupply periods, gross margins fall permanently: I was not able to find out why, but CoGS remains elevated above revenue while SG&A costs seem to normalize. It is not caused by more employees or a spur of CAPEX during the boom. One possibility is that it is caused by excess inventories.

High SG&A, high managerial compensation: SG&A as a proportion of gross profits is high, and unallocated expenses as a proportion of segment operating profits before overhead is also high. The company’s segments have a much higher margin before unallocated expenses than what the company shows at the bottom line. Management compensation is also high, according to the company’s 10-K for FY21, compensation for the three highest paying officers reached $2 million already. The company’s CEO has an agreement where he is entitled to receive 5% of the company’s net income as a bonus.

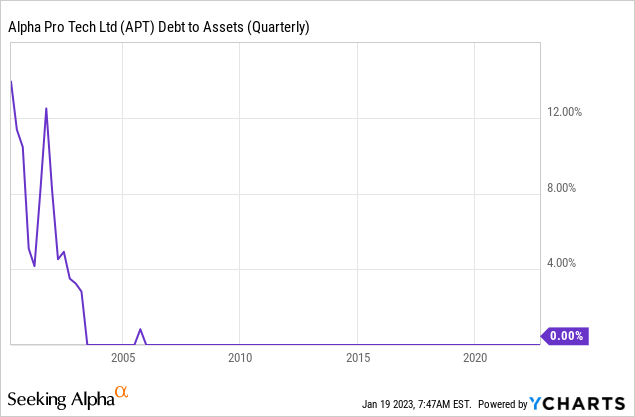

No debts: The company has sustained zero debts for most of its history.

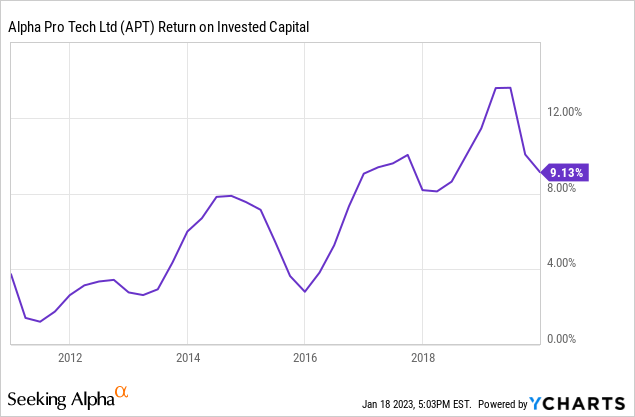

Share buybacks are the capital allocation strategy: APT has not invested too much in CAPEX, not even during extreme demand periods. It has not paid dividends either. Rather, it has consistently repurchased shares since 2010. This has halved the company’s outstanding shares count since. In turn this has increased ROIC.

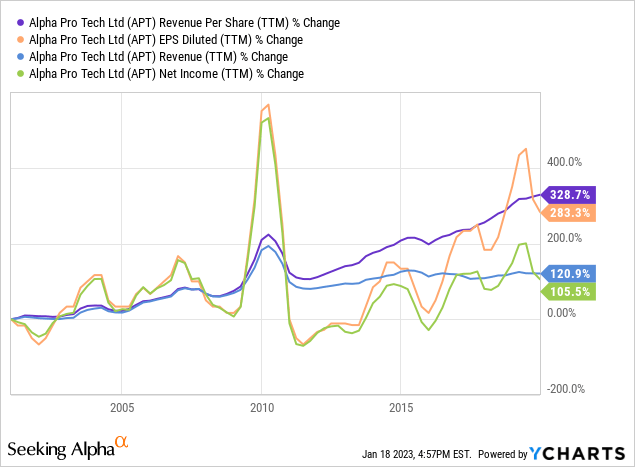

Share buybacks are an engine of EPS growth: Through the buybacks, the company has been able to increase EPS much faster than the speed at which it increases net income. In the chart below, going from 2000 to 2020 (before the pandemic boom), EPS had compounded at 5.3% annually. The compounding starting in 2011 is even higher.

No large owner, low management ownership: There is no large owner (above 10%) of the company’s stock. I usually prefer that companies have large owners, even more if the large owner has a managerial role (executive or director). It is common that a business without a large shareholder has a ratio of SG&A to gross profits that is high because there is not a lot of control. Management owns 13% of the company, but 9% of that is owned by a single director.

What awaits in the future

What will happen to gross margins: My biggest fear is the repetition of a 2010-2020 like period where margins are permanently below the previous level for some reason. The fact that I was not able to pinpoint it to a new factory, or more employees also makes me doubt. To make things worse, gross margins are currently below the pre-pandemic level and worsening.

Revenues seem to have stabilized for apparel: Revenues are not falling in nominal terms for apparel (which actually implies a real fall because of inflation). Still, they are falling sequentially since the beginning of the year and management commented on their 3Q22 earnings report that they expect lower demand ahead.

Will building supplies suffer from a construction cycle?: A recession or a downturn in construction can definitely affect the building supplies segment. I do not believe this is so bad though, for two reasons: first, it is very difficult and short-term looking to forecast this event; second, the company actually grew sales for every year between 2006 and 2012. In recent quarters, the company has mentioned that it continues to gain market share despite a decelerating demand.

Expected returns and valuation

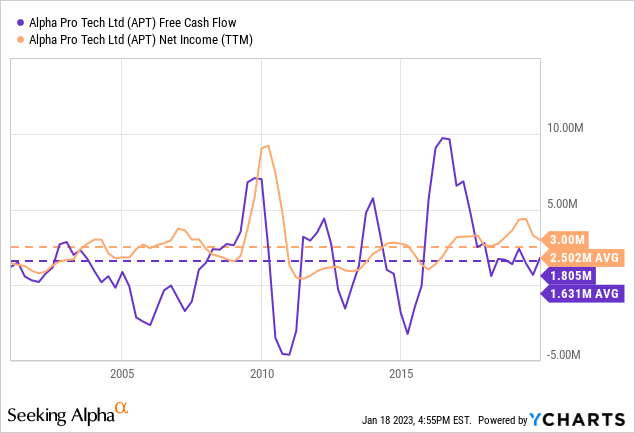

FY22E provides a normal return: If we do a simple back of the envelope calculation for FY22E where construction sales are somewhat slower during the second half, we arrive at about $4.6 million in operating income for the year. Without debts, and an average effective tax rate of 25%, this translates to $3.8 million, or a 7% expected earnings yield over the current $52 million market cap. Add 6% EPS growth across the cycle from the business supplies segment plus share buybacks, and we arrive at an expected return of 13%, not so bad.

A historical approach reveals a lower return: The problem is that the business is clearly cyclical, and it would be bad to ignore that coming out of a cycle top. It is difficult to predict if the company’s earnings have stabilized or if they will have a cyclical through. The historical approach reveals an average of $2.5 million in net income, or a 5% yield on the current market cap.

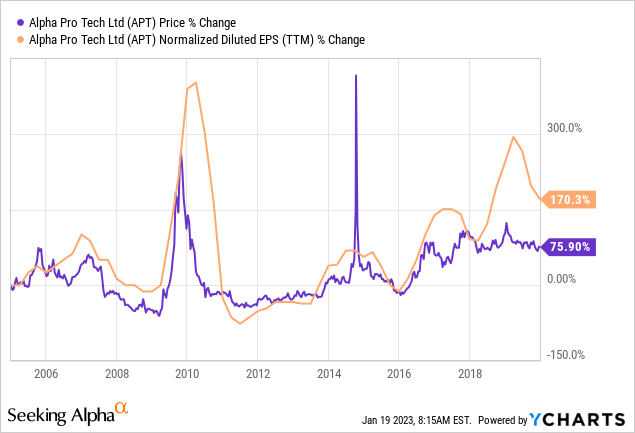

Is the business worth it?: Personally, I believe that risks are too high, mostly coming from operational leverage. The business quality is not great either, because the growing business supplies business is tied to a cyclical apparel business, and SG&A costs are high as well. Although the company has a great EPS growth engine through share buybacks, stock prices do not necessarily follow EPS growth.

Furthermore, considering the reduction in outstanding shares, the business seems to be trading at lower and lower market caps, compared to net income.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.