The latest official monthly household spending report showed a strong 6.3 per cent growth in November, reflecting a trend of increased spending during online sales such as Black Friday, and ahead of Christmas.

Throughout the year, spending was 11.4 per cent higher, but such spending fell for a fourth consecutive month, suggesting a peak in spending was well past.

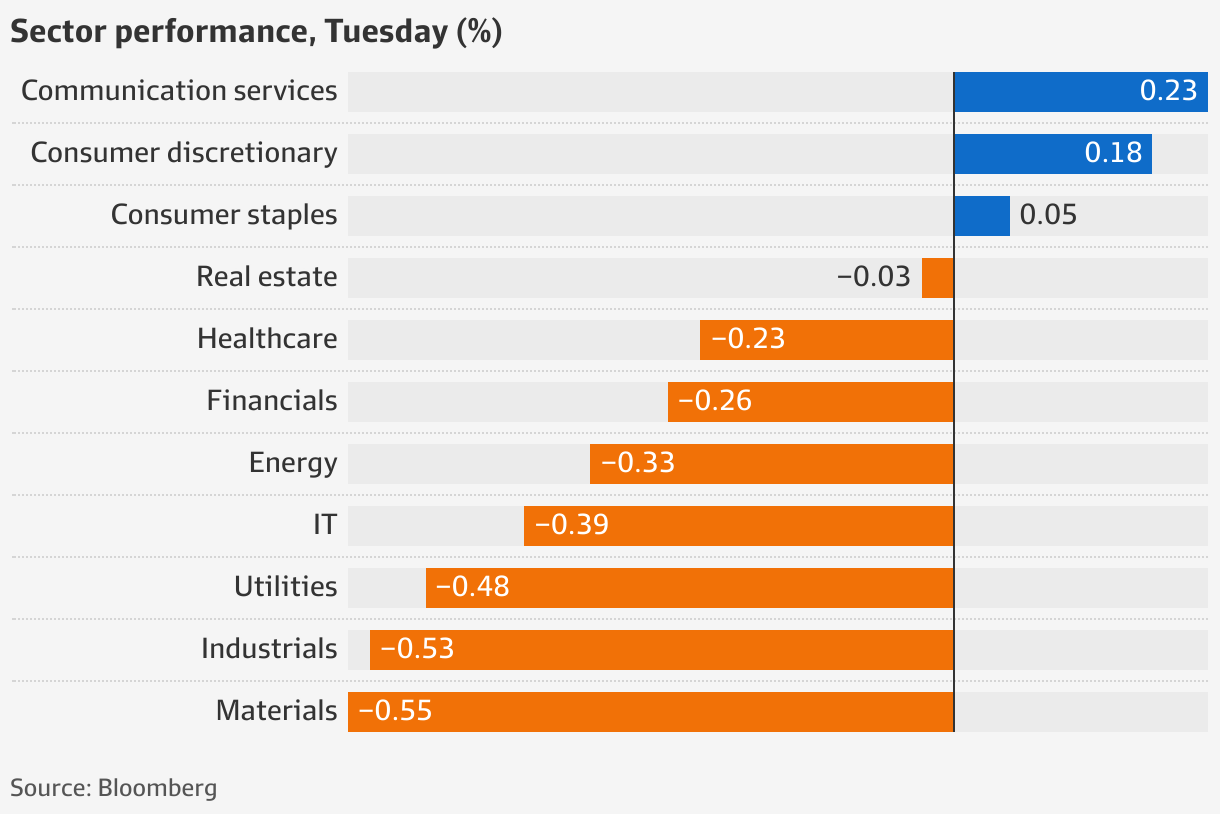

Discretionary retail was mixed.

Macquarie confirmed its preference for retailers with scale, market-leading and competitive brands, strong balance sheets, and exposure to low price points, in new research. It said youth categories were arguably best positioned in the current climate.

“December web site traffic data remains weak as retailers continue to cycle tough COVID comps. Online activity continues to moderate from elevated levels seen over CY20-21,” the broker said in a note.

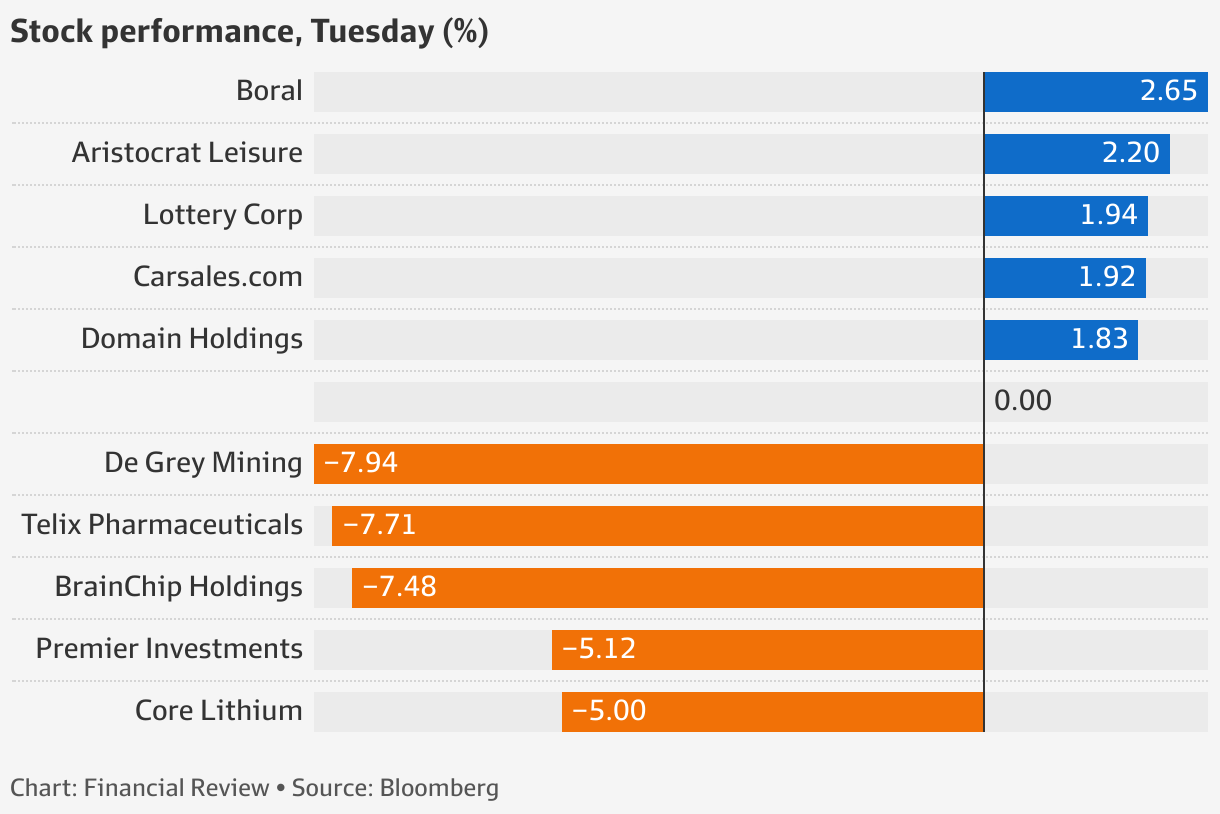

Premier Investments lost 5.1 percent to $24.85; Fashion accessories brand Lovisa dropped 0.3 per cent to $24.21.

Macquarie has “outperform” ratings on Lovisa with a price target of $27, and Premier Investments, with a target of $29.

Overall sentiment remains firmly in pessimistic territory, 21 per cent below the long-term index average, the latest ANZ-Roy Morgan consumer confidence survey showed.

If US consumer price data confirms the cooling seen in the most recent monthly jobs report, Atlanta Federal Reserve president Raphael Bostic said he would have to take a quarter point increase “more seriously and to move in that direction”, Reuters reported.

Wall Street’s St&The P 500 finished in the red on Monday, dropping 0.1 per cent.

Iron ore miners trimmed early losses and remained under pressure after China’s state planner vowed to ramp up efforts to regulate prices of the steel-making ingredient and crack down on “malicious” price speculation.

On the Singapore Exchange, the benchmark February iron ore futures contract was unchanged at $US117 a tonne.

BHP edged 0.4 per cent lower to $47.80, Rio Tinto shed almost half a per cent to $118.23 and Fortescue Metals firmed 0.7 per cent to $21.77.

Recce Pharmaceuticals rose 4.6 per cent to 68¢ after it received a grant intent from the Australian Patent Office for an antivirus agent. Recce is developing a new class of synthetic anti-infectives to address antibiotic-resistant superbugs and emerging viral pathogens.

The company said this would be the final patent, following those already granted in China, Japan, Europe and Hong Kong.

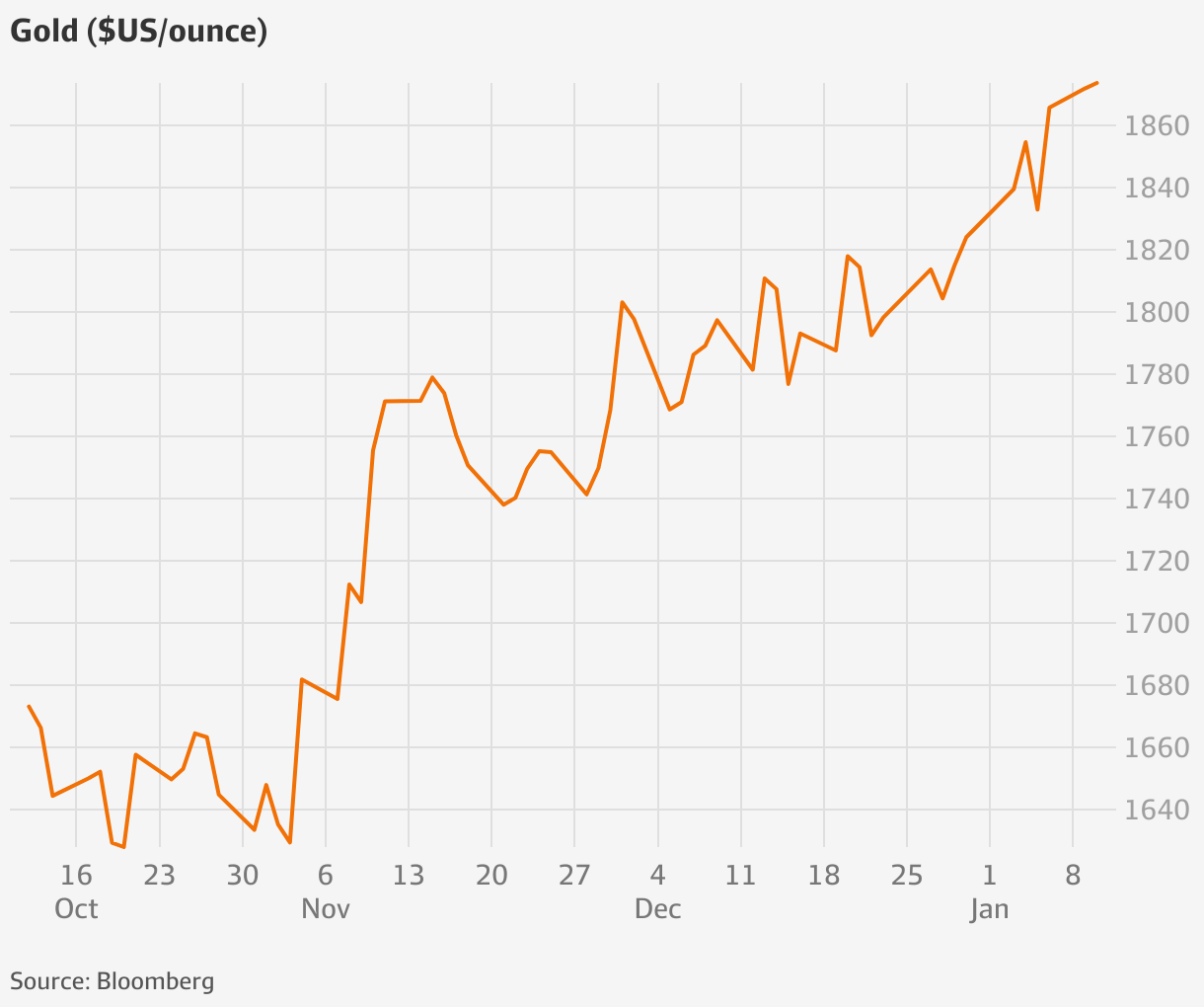

RBC Capital Markets has upgraded its gold price forecasts for this year, taking the precious metal to $US1735 an ounce, up 1 per cent from its previous prediction. For 2024, the broker expects gold to reach $US1700, or 1 per cent lower than its previous forecast.

Its $US1600 long-term forecast remains unchanged.

“We view a brighter macro backdrop ahead for gold, although prices have been resilient in the face of significant prior headwinds, and future upside may have already been front-run,” it said in a note.

“Forecast changes increase our Australian coverage FY23 EPS by typically 5 per cent-10 per cent and reduce FY24 EPS by around 5 per cent-10 per cent.”

RBC’s stock recommendations remain unchanged. It favors Northern Star Resources, King’s Resources, Bellevue Gold and St Barbara. It still expects underperformance from Evolution Mining.

Northern Star fell 1.9 per cent to $11.73, Regis Resources rose 0.5 per cent to $2.25, Bellevue dropped 2.2 per cent to $1.32 and St Barbara lost 5.7 per cent to 83.5¢. Evolution declined 2.4 per cent to end the day’s trading at $3.25.